“How to Calculate ATR?

The Average True Range (ATR) can be computed intraday, daily, weekly, or monthly and is typically based on 14 periods. The ATR in this case will be calculated using daily data. The initial 14-day ATR is the average of the daily TR values over the previous 14 days, and the first TR value is just the High minus the Low because there must be a beginning. Then, using the ATR value from the prior period, Wilder attempted to smooth the data.A copy

Current ATR = [(Prior ATR x 13) + Current TR] / 14

- Multiply the previous 14-day ATR by 13.

- Add the most recent day's TR value.

- Divide the total by 14

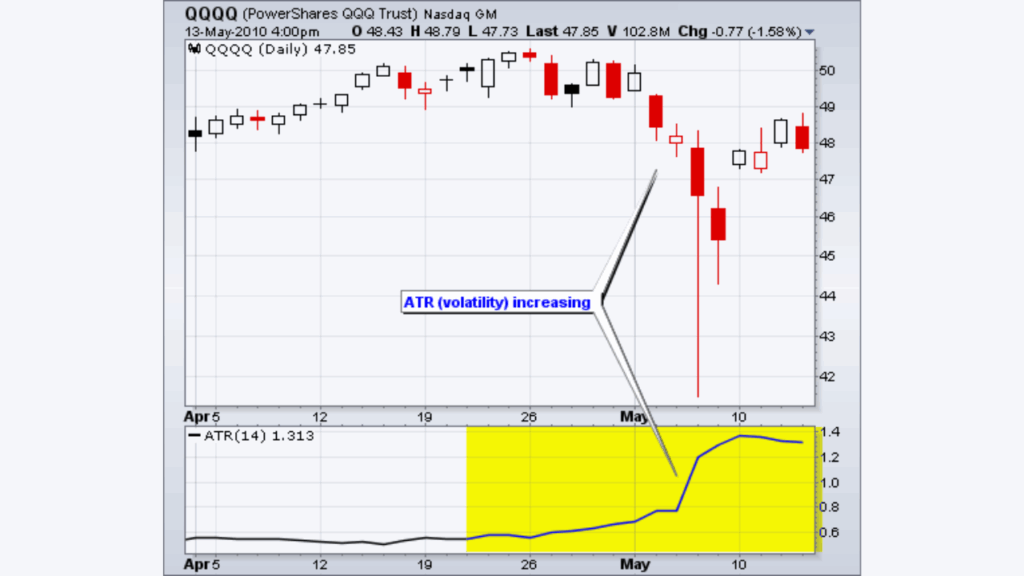

The initial True Range number (0.91) in the spreadsheet example is equivalent to the High minus the Low (yellow cells). The average of the first 14 True Range values (blue cell) was used to determine the first 14-day ATR value (0.56). The aforementioned formula was used to smooth subsequent ATR values. See how ATR rose when QQQ fell in May with numerous lengthy candlesticks; the spreadsheet values match the yellow region on the chart below.

ATR plotted on chart using StockCharts.com – Chart 1

There are a few things to keep in mind when attempting this at home. Initially, ATR values are dependent on how far back you start your calculations, exactly like with Exponential Moving Averages (EMAs). The first ATR is the average of the first 14 True Range values, while the first True Range value is the current high less the current low. On day 15, the actual ATR formula takes effect. Nevertheless, the effects of these initial two computations “linger” and have a minor impact on later ATR readings. A tiny fraction of data’s spreadsheet values might not perfectly match the price chart’s values. ATR values may also be marginally impacted by decimal rounding. We compute back at least 250 periods (usually much more) on our charts. ensure a much greater degree of accuracy for our ATR values.

Absolute ATR

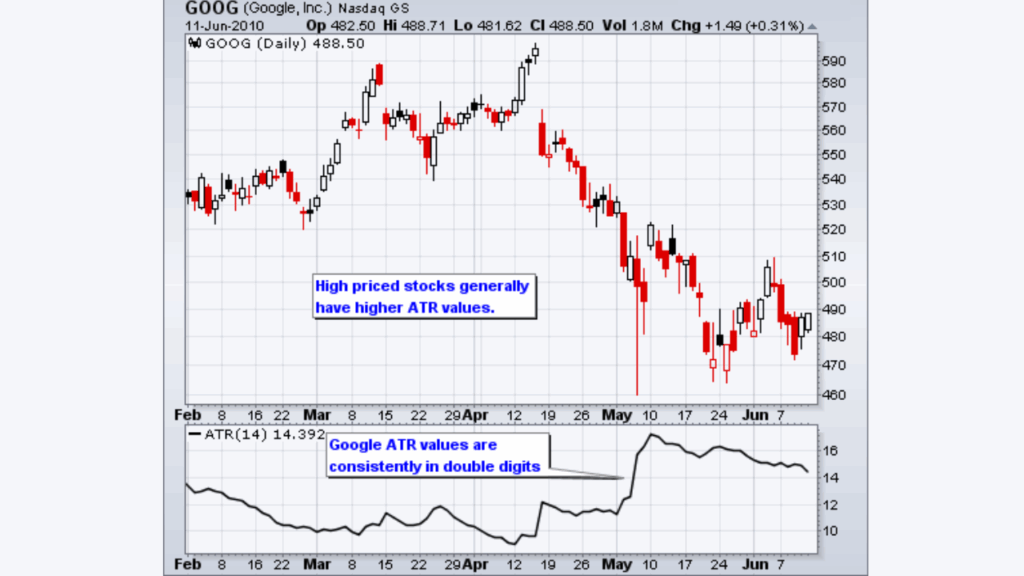

The True Range, which makes advantage of absolute price movements, is the foundation of ATR. As a result, ATR provides an absolute measure of volatility. To put it another way, ATR is not displayed as a percentage of the closing price. Therefore, compared to high-priced equities, low-priced stocks will have lower ATR values. For instance, the ATR values of a $20–30 security will be significantly lower than those of a $200–300 security. ATR values are therefore not comparable. Long-term ATR comparisons may not be feasible for a single security due to significant price swings, such as a drop from 70 to 20. Google has double-digit ATR values in chart 4, and Microsoft has ATR values less than 1 in chart 5. Their ATR lines are similar in shape even though their values differ.

you may be interested in this blog here: